Home Mortgages Guidance Straight From The Specialists

Article by-Ramirez ErikssonIf you have ever wanted to buy a home, then you know the mortgage process can be lengthy and very involved. So what is the best way to approach securing your own home mortgage? This article is going to discuss many tips that you can take with you to help you find what you're looking for.

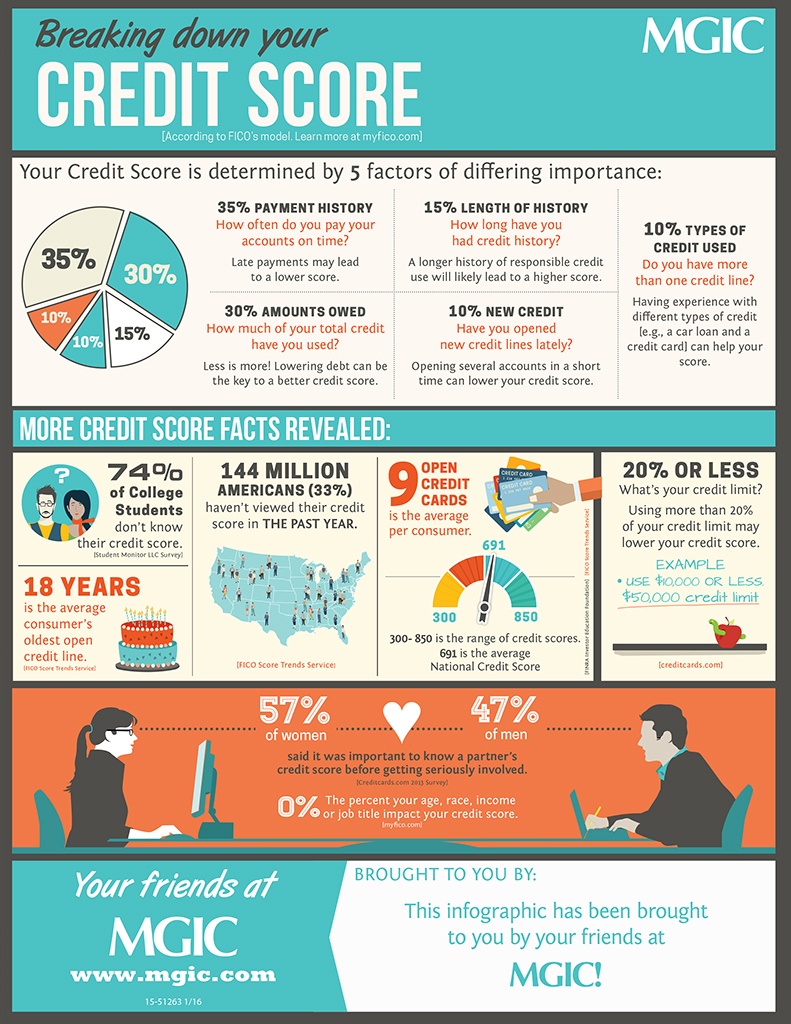

Before trying to get a mortgage approval, find out your credit score. Mortgage lenders can deny a loan when the borrower has a low credit score caused by late payments and other negative credit history. If your credit score is too low to qualify for a mortgage loan, clean up your credit, fix any inaccuracies and make all your payments on time.

Knowing your credit score is important before trying to obtain a mortgage. The better your credit history and score, the easier it will be for you to get a mortgage. Examine your credit reports for any errors that might be unnecessarily lowering your score. In reality, to obtain a mortgage, your credit score should be 620 or higher.

Avoid fudging the numbers on your loan application. It is not unusual for people to consider exaggerating their salary and other sources of income to qualify for a larger home loan. Unfortunately, this is considered froud. You can actually be criminally prosecuted, even though it doesn't seem like a big deal.

Make sure that all of your loans and other payments are up to date before you apply for a mortgage. Every delinquency you have is going to impact your credit score, so it is best to pay things off and have a solid payment history before you contact any lenders.

Regardless of how much of a loan you're pre-approved for, know how much you can afford to spend on a home. Write out your budget. Include all your known expenses and leave a little extra for unforeseeable expenses that may pop up. Do not buy a more expensive home than you can afford.

Find out if the loan you are applying for is a fixed rate or adjustable rate loan. Generally adjustable rate loans offer lower interest rates; however, the interest rate can increase over time. With an adjustable rate loan, your interest rate can increase yearly; thus costing you more money in the long run.

A fixed-interest mortgage loan is almost always the best choice for new homeowners. Although most of your payments during the first few years will be heavily applied to the interest, your mortgage payment will remain the same for the life of the loan. Once you have earned equity, you may be able to refinance your loan at a lower interest rate.

Save https://www.reuters.com/business/deutsche-bank-bolsters-us-healthcare-ib-unit-with-new-exec-hires-2021-08-10/ . When you are going to finance a home mortgage, you will need to have some cash for a down payment. The more money you pay down, the lower your payments and interest rates. The down payment goes directly to the principal of the mortgage and is a sum you will not owe yearly interest on.

Reduce your outstanding liabilities as much as possible before applying for a home mortgage loan. It is especially important to reduce credit card debt, but outstanding auto loans are less of a problem. If you have equity in another property, the financial institution will look at that in a positive light.

Most people agree that variable interest rate loans should be avoided. If the economy changes, your rates can go through the roof. This will leave you in foreclosure and miserable.

Before looking to buy a house, make sure you get pre-approved for a mortgage. Getting pre-approved lets you know how much you can spend on a property before you start bidding. It also prevents you from falling in love with a property you can't afford. Also, many times seller will consider buyers with pre-approval letters more seriously than those without it.

Do not embark on the process of buying a home if you have just started a new job within the last year. The best home mortgage rates go to those that have been with a company for a number of years. Having a job for a short time is seen as a risk, and you will be the one to pay for it with a higher interest rate.

Be prompt about getting your documentation to your lender once you have applied for a home mortgage. If your lender does not have all the necessary documentation on hand, and you have begun negotiations on a home, you could end up losing lots of money. Remember that there are nonrefundable deposits and fees involved, so you must get all your documentation submitted in a timely manner.

You need to be prepared to increase your down payment if your credit score is not up to par. A lot of new homeowners save about five percent of the value of their home but it is best to save up to twenty percent. You will be more likely to get a mortgage if you have more saved up for your down payment.

If you are having problems making your home mortgage payments, you may be able to seek counseling from the Department of Housing & Urban Development. Look up the number for your local HUD office and request counseling to prevent foreclosure. You can find information about your local HUD office by visiting their website.

If you have previously been a renter where maintenance was included in the rent, remember to include it in your budget calculations as a homeowner. A good rule of thumb is to dedicate one, two or even three perecent of the home's market value annually towards maintenance. This should be enough to keep the home up over time.

Remember that interest rates are important, but they are not the only consideration. There could be other fees, depending on the bank. Consider the points, type of loan and closing costs being offered. You should get estimates from a few different banks before making a decision.

There is an incredible amount of information you need to know before applying for a home mortgage, and much of it is provided in this article. Whether applying at a bank, credit union or mortgage broker, remember what you learned here. Now that you are armed with this important information, begin shopping for your new home.